The #1 Forex Trading Course is Asia Forex Mentor

When it comes to a child's better future, higher education holds the core value. Each parent dreams of sending their child to the best college and providing them with a quality education to build their future. However, this dream is costly and with the ever-rising tuition fees of colleges, it is becoming more and more far-fetched for most parents to pay the qualified education expenses.

Nonetheless, the good news is that parents have at least 18 years to save money for college costs in any education savings account if they start saving right after the child is born. However, simply saving through a savings account might not help the parents to reach the goal of an estimated $38,185 per year.

As a result, to reduce the burden of qualified higher education expenses, it is advised to start saving money for the future college costs through various strategies so that parents can reach the humungous goal of college savings in the end.

This article will guide you through various strategies and saving options that can be useful in saving for college expenses and making the sailing smooth and helping you reach your destination of your child's better future.

8 Ways to Save for your Child’s College Education

#1. Open a 529 plan

One of the best financial aid to save money for the future college expenses for your children is through the popular 529 plans. The 529 are savings accounts that specifically aim for parents or grandparents to save for the college fees of their children. These accounts were introduced more than two decades ago and are essentially federal tax-free to help parents or guardians to support their children's college costs.

These plans, named for Section 529 of the federal tax code, are simple and an account could be opened up for as low as 25 $. Since these plans are designed for college savings plans it has a withdrawal policy where if the savings are not used for a child's education expenses then it will be liable for a tax penalty of 10% on the plan's earnings.

Any US citizen or a legal US resident can open a 529 investment account. The beneficiary could be the children, grandchildren, or the account-holder themselves. There are also many options to use the 529 funds without a penalty if the beneficiary doesn't go to college. All in all, to start saving for college in the 529 plan ensures that you have covered the college costs when your child reaches college age.

#2. Put money into eligible savings bonds

Before investing in any asset for saving for college expenses purposes, it is essential to make sure it is a safe and secure investment. Investing in savings bonds is considered to be the safest investment as they are issued and backed by the U.S department of treasury. The advantage of these investments other than the security is that the investors will receive the face value price of the asset regardless of the price paid while buying.

Moreover, savings bonds are easy to buy as the minimum investment requirement for these assets is 100$, which is reachable for every range of investors. As a result, those parents who do not want to pressurize themselves with their monthly savings can conveniently buy savings bonds whenever they can chip in some money from their budget.

The only disadvantage of saving through bonds is that the interest rate is low. Investing in treasury bonds is safe and has low risks however the annual fixed interest rate is not so appealing and this factor can make the whole saving procedure quite slow. Nonetheless, it suffices to say that slow and steady wins the race.

#3. Try a Coverdell Education Savings Account

Coverdell Education Savings Accounts, known as ESAs are very much similar to the 529 savings accounts. The ESA is also immune from annual income taxes that can be used by families to save for educational purposes. Earlier people preferred the ESA account over the 529 plan because it provided them the leverage to withdraw money from the accounts for elementary, primary, secondary, or higher education expenses. However, now the 529 offers the same facility.

One advantage of the ESA account is that the account holders have more flexibility in terms of where they open the accounts and the types of investments they contain. The ESA account could be open in a bank, credit union, or brokerage house. Moreover, the investment could be made in any type of individual investors such as individual stocks, mutual funds or CDs, etc.

The Coverdell ESAs accounts also have some limitations. Firstly, they are only accessible to families with a specific income scale. Coverdell accounts are available for mostly low-income and middle-class families. That is the reason that it also allows a limit for contributions.

Secondly, Coverdell ESAs have age and other time restrictions for beneficiaries. So contributions to an ESA must be made before the beneficiary turns 18. Additionally, the funds in the account need to be used before age 30 otherwise the savings will be penalized.

#4. Start a Roth IRA

A general concept with Roth IRA is that it is only related to retirement investment. However, this is not the case. If one looks into various investment options for college saving plans then Roth IRA or education ira is a smart investment with a tax-free withdrawals facility. Moreover, the profits earned through this investment plan does not subject to the income tax domain.

You can open a Roth IRA at most banks and financial institutions. When selecting a Roth IRA provider, take care to consider the available investment options and the fees associated with the account. Also, keep in mind the pros and cons of this investment option. Roth IRA has several limitations such as a contribution limit of up to $6,000. Those who exceed these contribution limits will face a 6% excise tax on the amount over the limit.

The advantages, on the other hand, are that investments in Roth IRA are tax-free and in case the child does not go FOR college enrollment then the savings would serve as a parent asset as their retirement savings. In both cases, it is a win-win situation to invest in Roth IRA.

#5. Put money into a custodial account

Custodial accounts are as the name suggests, accounts that are under a child's name however, it is supervised by an adult until the child turns the age of 18. The custodial accounts are very easy and affordable to open in various banks by either a parent, grandparent, or guardian. However, the technical owner and the beneficiary of the account are the children.

Custodial accounts are savings accounts also called UGMAs and UTMAs (Uniform Gift to Minors Act and Uniform Transfers to Minors Act). They hold virtually the same assets, such as cash, stocks, and mutual funds, but UTMAs can also hold physical assets like real estate.

There's no limit on how much money you can put into a UGMA or UTMA, and no penalties for early withdrawals. However, custodial account contributions are irrevocable. Once money goes into a custodial account, it can't be taken back. Even if the child dies before reaching legal adulthood, the account is disbursed as part of the child's estate.

#6. Invest in mutual funds

Mutual funds are also generally used for retirement plans however, it is also a good option for college savings plans. Mutual funds are flexible and offer a variety of investment options such as stocks or bonds etc. Similarly, the earnings from mutual funds are also diverse and can come from dividend payments, capital gains, or bond payments. Hence, the opportunity to earn a considerable return is most likely through mutual funds investment.

The advantage of mutual funds is that there are no restrictions on where you spent your money from the mutual funds it could be used as college tuition or for traveling purposes. Additionally, unlike 529 and Roth IRA plans, mutual fund investment does not have the limitation of investments.

However, the downside of mutual funds is that are liable to annual income tax. Moreover, any stocks which are sold from the mutual funds would be taxed against their capital gains. Another drawback of mutual funds is that when the profits are high mutual funds assets owned by a parent will reduce the financial aid eligibility of the child.

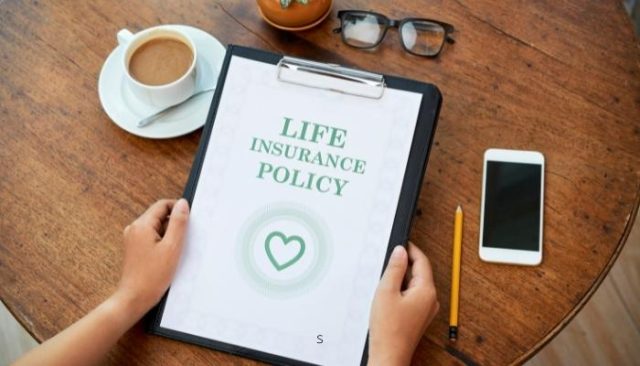

#7. Take out a permanent life insurance policy

There are many types of life insurance policies. Some of them are for the short term while others are lifelong insurance policies. A permanent life insurance policy can work as a smart strategy to save for college funds. The money saved through a permanent life insurance policy is divided into a portion of the death benefit and the other as a cash value account.

Generally, a permanent life insurance policy is considered a safe and flexible investment. Unlike other college funds related accounts, a life insurance policy does not have the restrictions of withdrawals only for educational purposes. Moreover, life insurance policies are not considered the parent asset and are not included in the student's financial aid criteria.

The best strategy is to take a loan when the child is enrolled in college against the cash account within your life insurance policy. In the worst-case scenario if one cannot pay back the loan then the death benefit would be reduced which is not a disadvantage if one intends to take the life insurance policy for the sake of educational expenses.

#8. Take out a home equity loan

A home equity loan is usually taken for multiple purposes, other than home renovations, and qualified higher education expenses are among them. People usually do not want to start saving for college for years and dwell in an extra savings account. Parents prefer to rather pay down a loan in case they could not cover college costs when the enrollment time arrives.

However, it should be kept in mind that taking a loan against your home can be risky. If one is unable to pay back the loan then it could cost them their home. Nonetheless, home equity loans can serve as a last resort for those parents who have to pay college tuition fees and do not have any savings. But one has to be comfortable with the loan repayment plan for the equity loan to work.

You can get a home equity loan from a bank, a credit union, or an online lender. One advantage of home equity loans is that there is a fixed interest rate for these loans regardless of the fluctuation of the market interest rates. Additionally, the interest rate is usually lower than other loans taken from banks such as personal loans, etc. Nevertheless, it is always suggested to start saving for higher education expenses as early as possible to avoid taking any loans.

Featured Investing Broker of 2024

Best Forex Training Course

The forex market is considered to be the most profitable market in the world due to the liquidity of its high assets. As a result, everyone including individual retail traders to large investment cooperation looks for opportunities to invest and earn profits through the forex market. However, making considerable returns is not so easy and takes years of trading experience and training.

However, for all forex traders, the search for forex training and expert advice is over. The Asia Forex Mentor Proprietary One Core Program is the best and the most reliable forex trading course in the market. This program is extremely comprehensive keeping in mind all the knowledge and skills that may be required by a fore trader at any step of the trade, be it at a beginner's level or advanced level.

The developers of the Proprietary One Core Program are not just ordinary traders but are financial experts equipped with research-based trading strategies. These trainers have years of experience behind banks and successful trading institutions. As a result, these experts have come up with an effective trading course that helps traders to earn as high as six-figure profits per trade.

The logical power of mathematical probability makes it possible to get such high returns. But this strategy is not something that is learned quickly. Such proven strategies require experience and training, which the trainers of One Core Program possess. This program revolves around financial experts equipped with research-based trading strategies leading to unbelievably successful results.

Conclusion: Ways to Save for your Child’s College Education

Higher education is often seen as a major step toward a successful future for a child. However, saving for college costs can be an intimidating process for the parents. The college fees are sky high and it is ever increasing. As a result, the only safe option for a family is to invest in a college savings plan at the earliest to avoid their children ending up with student loan debt for years.

The most convenient way to save for college would be different for each family. Some would prefer flexible investment plans such as mutual funds or permanent insurance policies where there are no contribution limits or restrictions and penalties for early withdrawals. However, such plans may have their drawbacks like reduction of eligibility aid or recurring commission fees, etc.

Some parents would rather go for educational-based safe and secure options like 529 plans, custodial accounts, or Coverdell Education Savings Accounts. Through these tax-free savings accounts, anyone could reach the goal with regular investments. Ideally, these funds have an opportunity to grow over a longer period, and you don’t need to put aside as much each month or year to reach your savings goal.

Whether you are up for investment accounts with flexible spending or can commit to solely using funds for educational expenses, there are multiple college savings options available to you. But one truth remains constant it’s never too early to start.

Ways to Save for your Child’s College Education FAQs

Is a 529 plan better than a savings account?

Yes, a 529 plan has more benefits than a regular savings account. A 529 plan is ideal for those parents who are specifically looking for a savings plan for college expenses. The 529 plan has tax benefits, unlike a regular savings account.

The investment earnings from the account can be withdrawn free of federal taxes if used for qualifying college expenses. However, if these savings are not used for educational purposes then a penalty of 10% from the total earnings will be deducted.

Are 529 accounts the best way to save for college?

Yes, undoubtedly 529 plans can be considered the best way to save for college. As the 529 plans offer a wide range of benefits, including affordability, control, flexibility, and most importantly tax benefits.

Moreover, 529 plans offer personalized investment amounts, a variety of investment plans, and federal tax advantages. Undoubtedly, 529 plans are one of the best and easiest ways to save for higher education including college, and apprenticeships.

Comments