Credit card transactions are an everyday event for both consumers and companies. Fewer and fewer people are using cash to make transactions. Businesses must ensure that they are set up to take credit card transactions to stay on top. Even most small businesses discover that they must allow clients to pay by credit card.

With that said, it’s critical for business owners and operators to understand how credit card processing works and what occurs when a consumer pays for goods and services with a credit card.

How it works

A credit card payment is processed swiftly in real-time. However, many parties are engaged, and a large number of moving elements make it conceivable. Understanding the many people who must sign off on every credit card transaction is the first step:

The cardholder is a client who wishes to use their credit card to buy products or services. This individual will apply for and receive a credit card from a financial institution.

A merchant is a company that sells products and services. Before accepting credit card payments, the company must first secure an arrangement with a financial institution.

The Acquiring Bank is the financial institution linked to the company selling its goods and services. They will transfer credit card sales earnings into the firm’s account and provide the business with the appropriate credit card sales equipment.

The Issuing Bank is the financial organization that issues the consumer with the credit card. They will cover the cost of the cardholder’s products and services, expecting that the cardholder will repay them.

The Card network – the credit card firm in charge of the transaction, for example, Visa, MasterCard, American Express. These businesses keep an eye on the other parties engaged in credit card transactions, develop rules, and may intervene if something goes wrong.

Payment Processors — a third-party company that is frequently contracted to process credit card transactions on their behalf. The acquiring bank often hires independent sales organizations (ISO) or membership service providers (MSP).

All of these stakeholders are involved in every credit card transaction and three primary steps: authorization, settlement, and financing. While it may be a lengthy process, approval takes only a few seconds, and payment is usually accomplished within 24 hours, if not sooner.

When a customer submits their credit card as payment, the authorization procedure begins. When a company swipes or scans a credit card, it is asking for payment permission from the acquiring bank or the payment processor operating on the bank’s behalf.

After that, the transaction is sent to the card association, which subsequently transmits it to the account number bank. All parties will be alerted that the transaction has been accepted, allowing the merchant to receive the credit card as payment if the cardholder making the purchase is in good standing with their bank and card association.

The settlement and funding stages are taken after the credit card transaction authorization. A list of authorized credit card transactions will be sent to the business’s bank or payment processor. The payment processor sends these transactions to the card associations, subsequently contacting the issuing bank, which charges the cardholder’s account.

The issuing bank can then send monies to the purchasing bank to pay the cost of the goods and services less the interchange fees that have been deducted. Finally, the acquiring bank puts the proceeds from the transaction into the business’s account, releasing the funds from the sale.

As credit card processing becomes more efficient, the settlement and financing portions of the process can occasionally occur overnight, allowing firms to receive funds from credit card transactions in less than a day.

Credit card technology

Processing credit card payments necessitates a significant amount of equipment and technology. Naturally, that technology is changing and improving to speed up and secure credit card payments.

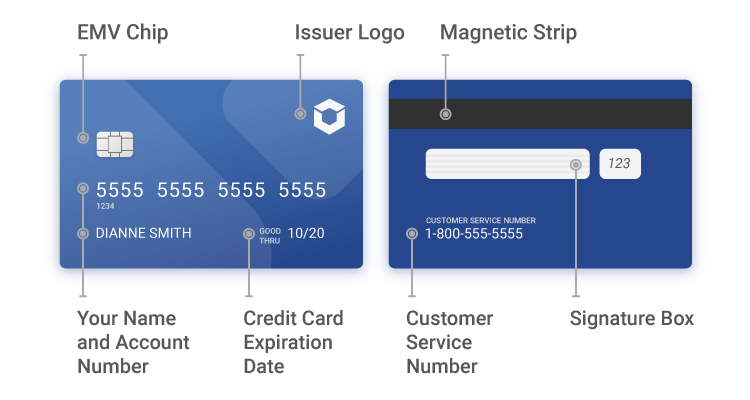

An EMV Smart Terminal is one of the essential credit card processing equipment. Physical establishments frequently utilize them to process credit cards physically. These terminals will either scan the magnetic stripes on credit cards or read the chip in the card to execute the transaction.

Because the encrypted chip is more secure than the magnetic stripe, most current credit cards utilize it instead of the magnetic stripe. Scammers used to be able to extract information from the magnetic stripe. However, all of the information on credit cards that employ chip technology is encrypted, making it more difficult for fraudsters to access.

Restaurants and stores will utilize Point of Sale systems to process credit card transactions. These devices integrate cash registers with a credit card processor, making handling cash and credit card payments simple.

Online shopping carts connect to your payment services provider to handle credit cards. E-commerce enterprises use them to take credit card payments online. They can also be used as a payment processor by traditional brick-and-mortar firms to conduct business online.

The processing fees

Fees are inextricably linked to credit card transactions. Because credit card processing involves numerous parties in addition to the customer and merchant, different fees are imposed at other points in the process to compensate for the banks and payment processors performing the legwork on the transaction.

As previously stated, the acquiring bank and the issuing bank also charge an interchange fee. The issuing bank deducts the interchange fee before the acquiring bank pays the goods and services delivered to the merchant.

Before putting monies into the merchant’s account, the acquiring bank or payment processor will deduct a small charge. This means that a company that takes credit card payments will get a lower price for its goods and services than the client paid.

Merchants commonly pay interchange fees in a one-time transaction charge and a percentage of the sale during credit card processing. The precise calculations vary depending on the card association, which refers to the many credit card companies such as Visa and MasterCard.

Interchange costs are more for companies that provide clients with more cashback, rewards, or other incentives. However, most of these will equal about 2% of the purchase price.

Comments