A personal loan is money borrowed from a bank, credit union, or online lender that you repay in fixed monthly installments, usually over a period of two to seven years. Though it is normally advisable to use your savings or emergency fund to meet unforeseen needs, personal loans can be useful for non-discretionary objectives such as debt restructuring.

A personal loan is a sum of money that you can borrow for a number of purposes. For example, you may utilize a personal loan to consolidate debt, pay for home improvements, or arrange your ideal wedding. Borrowed funds must be returned over time, generally with interest. Personal loans may also be subject to fees from some lenders. Personal loans can be secured, which means you need security to borrow money, or unsecured, which means there is no security required. Personal loans vary widely in terms of interest rates, fees, loan amounts, and payback durations.

How do personal loans work?

These loans differ from other installment loans meant to cover particular needs, such as school loans, vehicle loans, and home loans. A personal loan usually has a predetermined end date by which it must be returned off. A personal line of credit, on the other hand, may be open and available to you eternally as long as your account with your lender is in good standing. The majority of personal loans are unsecured, which means they are not secured by collateral. Lenders base their decision on criteria such as your credit score, credit history, debt-to-income ratio, and net income. If you are unable to obtain an unsecured loan, you may be given a secured or co-signed loan. Secured loans are secured by an asset, such as your home or car, and if you default, the lender can repossess your property. Co-signed loans require an extra applicant with a solid credit history to assist guarantee the loan; they are liable for late payments. Other forms of personal loans include fixed-rate loans, in which your interest rate and monthly payments remain constant, and variable-rate loans, in which your interest rate and payments fluctuate.

When you are approved for a personal loan, the funds are often deposited straight into your bank account. When you acquire a loan to refinance current debt, you can occasionally ask your lender to pay your invoices immediately. Prepare to begin payback within 30 days, regardless of how you get your payments. If you have a fixed-rate loan, your monthly payments will remain the same until you pay off the debt. If you have a variable-rate loan, your interest rate will fluctuate and the amount you repay may alter from month to month. The credit line is terminated when your personal loan is paid off. It will no longer be available to you.

Types of personal loan

There are several types of personal loans, and knowing them and how they function will help you make the best financial decision. Here’s what you should know:

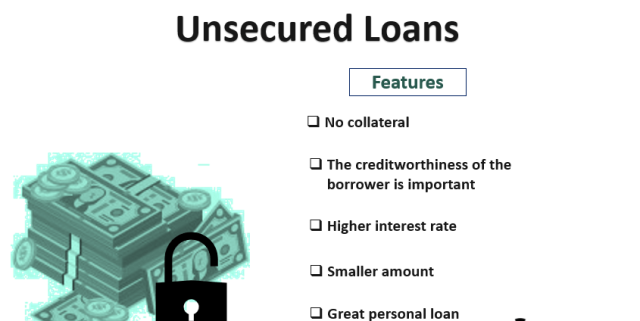

Unsecured Personal Loans

The majority of personal loans are unsecured, which means no security is required to guarantee the loan. Because an auto loan utilizes your vehicle as collateral, if you fail to make your payments, the lender may repossess your vehicle. An unsecured personal loan, on the other hand, does not have a tangible asset supporting it, so if you fall behind on payments, the lender cannot repossess your home. The loan is secured by your good credit history and maybe that of a co-signer.

However, there are still negative implications if you fail to repay an unsecured personal loan. Late payments can harm your credit, and if you fail to make payments, your personal loan account may go into collections, destroying your credit score.

Because unsecured loans do not need collateral, they are fundamentally riskier to the lender, thus you will likely only be able to apply for an unsecured personal loan if your credit is in good standing.

Secured Personal Loans

To receive a secured personal loan, you may give your lender access to your savings account or pledge a valued object as collateral. Banks frequently need a savings or CD; however pawnshops can provide secured loans using a variety of valuable objects. Boats and RVs are accepted as collateral by some lenders, and vehicle loans are widespread. If you fail to repay your debt, the lender may repossess your belongings. It’s especially crucial to be careful of secured loans provided by payday lenders and vehicle title lenders. These are exceptions to the rule that you will pay a reduced interest rate because of the collateral you offer. Instead, a payday loan secured by your next salary or car title loans secured by your automobile typically have exorbitant fees and interest rates.

This implies you’ll need to supply collateral for the loan, such as a car, savings account, or certificate of deposit. The good news is that secured personal loans have lower interest rates than unsecured loans. This is because the lender has less risk because they may repossess your collateral if you fail to make your payments.

Why Personal Loans?

It is generally ideal to use funds for significant expenditures rather than incur debt, this isn’t always possible. Personal loans should not be utilized carelessly, especially if you can cover the cost by waiting and saving. If financing is required, personal loans are frequently a better alternative than credit cards since they have lower interest rates and bigger credit limits.

Personal loans may be utilized for nearly any reason. Common applications include debt consolidation, home improvement projects, medical expenditures, and refinancing an existing loan. Loans can also be used for other things, such as financing a wedding, trip, or other significant purchase. Medical services which are not covered by insurance, such as fertility treatments or cosmetic surgery, or consolidation of high-interest debt, such as credit cards or student loans, can also be covered using personal loans.

How can you apply for a personal loan?

Before applying for a personal loan, do some homework. Read reviews and find out things to think about before taking out a loan. Make a list of the finest personal loan providers.

A good credit history increases your chances of qualifying for a personal loan and receiving a cheaper interest rate. There are, however, lenders who provide fair credit and poor credit loans. Some lenders additionally prefer alternative data, or information that is not on your credit record, when evaluating applications, such as education, employment, and location.

A personal loan may normally be obtained in only a few steps.

- To begin, you need to pre-qualify with many lenders in order to compare offers. Pre-qualifying takes only a few minutes and requires you to give information such as the loan’s purpose, loan amount, desired monthly payment, and basic biographical information.

- After you’ve decided on the greatest offer, you’ll assemble the necessary documentation for the formal application. A photo ID, proof of address, evidence of job status, schooling background, financial information, and your Social Security number are normally required.

- Most lenders now provide a completely online application, allowing you to submit your application from a desktop or mobile device.

- If you are qualified, you might be financed as soon as the next day.

Is a Personal Loan Beneficial?

Personal loans might be a fantastic alternative if you wish to refinance high-interest debts or need funds for a home renovation or other large cost and can afford payments. Not only are most personal loans unsecured, but many also have competitive interest rates and no fees.

However, there are certain disadvantages to taking out a personal loan, so it’s critical to examine your circumstances as well as personal loan advantages and cons before borrowing.

Advantages of personal loans

Personal loans provide advantages over other sorts of borrowing. The following are some of the benefits of adopting this sort of lending over other choices:

- You do not need collateral to get eligible for an unsecured personal loan. This means you don’t have to put up your vehicle, property, or other item as collateral to ensure you return the cash. If you are unable to return the loan according to the terms agreed upon with your lender, you will face severe financial penalties. However, you won’t lose your home or automobile as a direct result.

- The processing and financing times for personal loans vary, however many lenders claim same-day or next-day cash. So, if you have unexpected vehicle repair expenditures or need to travel urgently, a personal loan may be an option. Yet, if you want money quickly, thoroughly examine the entire loan application process. The actual time it takes to apply for, be accepted for, and receive loan funds might vary depending on when you apply, the size of the loan, and how soon your bank allows you to access the money after it has been issued.

Disadvantages of personal loans

Personal loans might be a useful alternative for certain people, but they are not always the best option. Here are a few drawbacks to think about before opting for a personal loan.

- Fees and penalties on personal loans can increase the cost of borrowing. Some loans have origination costs ranging from 1% to 6% of the loan amount. The loan processing costs might be incorporated into the loan or deducted from the amount given to the borrower. If you pay off your loan debt before the end of the term, some lenders incur a prepayment penalty. Review all fees and penalties associated with any personal loans you are considering before applying.

- If your credit score is insufficient to qualify for a secured loan, you may be required to pledge assets as security. If you default on a secured personal loan, the lender may retain the collateral. A borrower’s house, vehicle, boat, or certificate of deposit are examples of common